Usually we would plot the data before applying a forecasting algorithm. However, we have already done this. We know from before that the process is stable, that is, random fluctuations around the center.

Use the simple exponential smoothing function, ses(), from the forecast package to forecast the time series five quarters ahead. Save the output in the object fit. Because the output was directed to an object, for future reference, there is no output at the R console.

fit <-ses(Y3_ts, h=5)

Examine the model parameters, which for simple exponential smoothing, is \(\alpha\). The algorithm chooses the value of \(\alpha\) that minimizes the mean of the squared errors.

The smoothing algorithm chose an extremely low value, \(\alpha\) = 0.0001. The reason is that the process is stable, consisting of nothing more than random fluctuations about the same mean with a constant level of variation. With pure randomness, there is no gain from referencing forecasting error from the current time to adjust the forecast for the future time. All data values result from random fluctuation about the mean. Hence, \(\alpha \approx 0\).

Display the contents of the fit object to view the forecasts.

fit

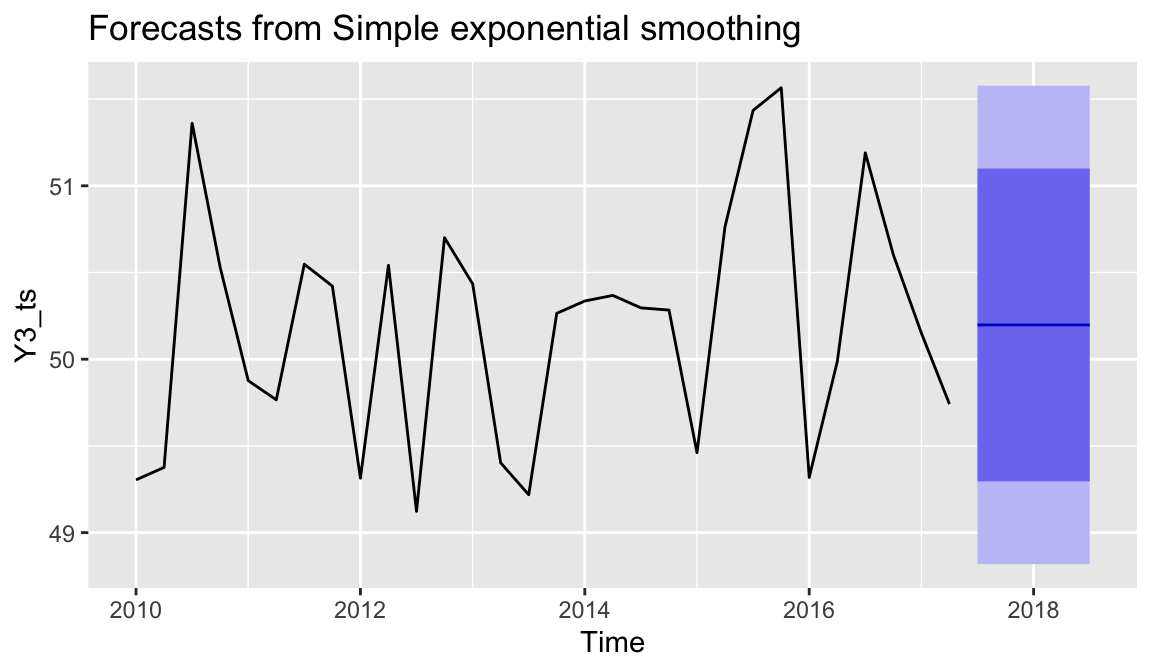

Point Forecast Lo 80 Hi 80 Lo 95 Hi 95

2017 Q3 50.19771 49.29586 51.09955 48.81846 51.57696

2017 Q4 50.19771 49.29586 51.09955 48.81846 51.57696

2018 Q1 50.19771 49.29586 51.09955 48.81846 51.57696

2018 Q2 50.19771 49.29586 51.09955 48.81846 51.57696

2018 Q3 50.19771 49.29586 51.09955 48.81846 51.57696

Because the process is stable, each forecasted value is the same, a value very close to the mean of Y3, \(m\) = 50.189.

With the autoplot() function, plot the data and the forecasts, with the 80% and 95% prediction intervals.

autoplot(fit)

For this stable process the prediction intervals essentially span the range of the data. The forecast indicates properly indicates that the next value of the time series will likely lie within the specified range of data centered over the mean.

4.2 Forecast from Trend + Seasonality

With this example, begin with a time series characterized by both trend and seasonality, as seen from a previous homework.

d <-Read("http://web.pdx.edu/~gerbing/0Forecast/data/Sales07.xlsx")

[with the read.xlsx() function from Schauberger and Walker's openxlsx package]

Data Types

------------------------------------------------------------

character: Non-numeric data values

integer: Numeric data values, integers only

double: Numeric data values with decimal digits

------------------------------------------------------------

Variable Missing Unique

Name Type Values Values Values First and last values

------------------------------------------------------------------------------------------

1 Year integer 16 0 4 2016 2016 2016 ... 2019 2019 2019

2 Qtr character 16 0 4 Winter Spring ... Summer Fall

3 Sales double 16 0 15 0.41 0.65 0.96 ... 2.11 2.25 1.74

------------------------------------------------------------------------------------------

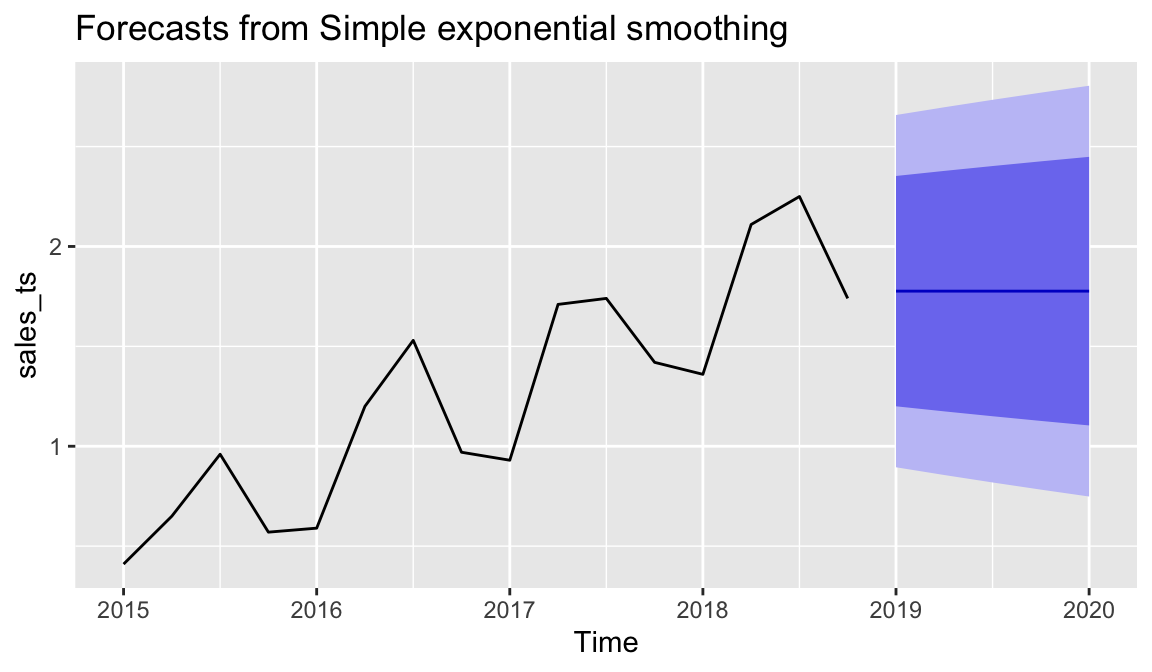

Simple exponential smoothing does not account for trend and seasonality, and so does not apply to this time series. To illustrate the mismatch, apply this forecasting procedure to these data, again with the ses() function from the forecast package.

To illustrate the parameter alpha, first set \(\alpha=0.3\).

fit <-ses(sales_ts, alpha=.3, h=5) fit$model # model parameters

The reported value of sigma is the standard deviation of the residuals of the component of output called model that the ses() function created. Here, \(s_e=0.450\). Compare this value across models to better understand which model is functioning more effectively.

View the forecasted values and corresponding prediction intervals, and plot.

fit

Point Forecast Lo 80 Hi 80 Lo 95 Hi 95

2019 Q1 1.7764 1.199957 2.352842 0.8948068 2.657993

2019 Q2 1.7764 1.174576 2.378224 0.8559897 2.696810

2019 Q3 1.7764 1.150223 2.402577 0.8187447 2.734055

2019 Q4 1.7764 1.126782 2.426018 0.7828950 2.769905

2020 Q1 1.7764 1.104158 2.448642 0.7482946 2.804505

autoplot(fit) # visual forecast

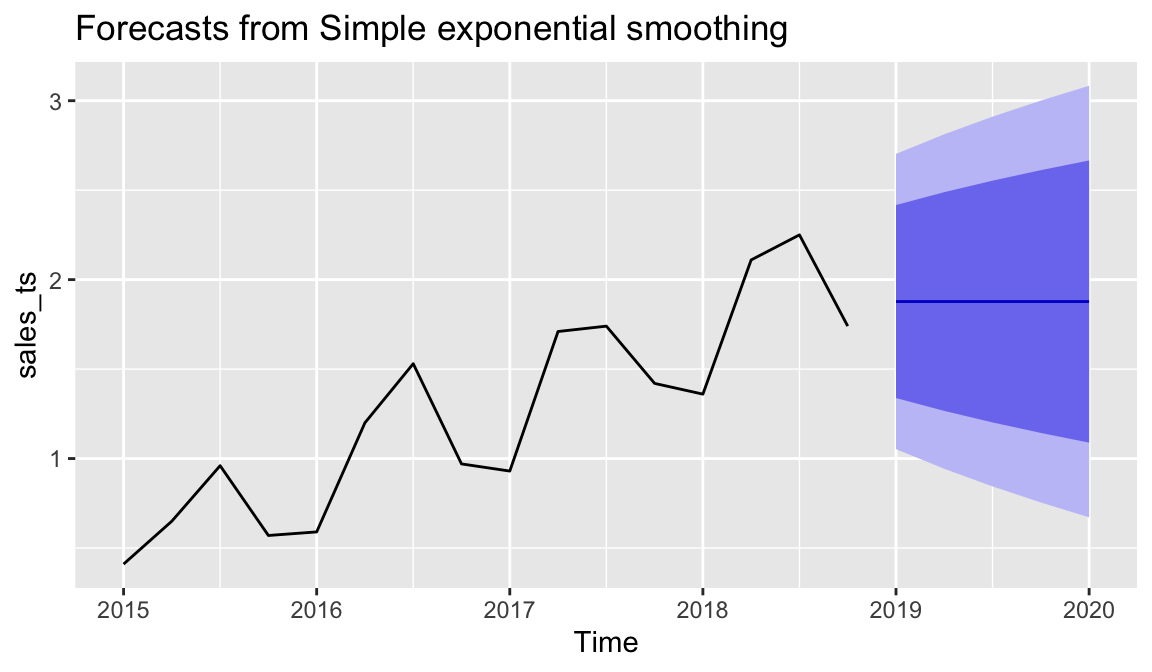

Here let ses() choose the value of \(\alpha\) that yields the best fit to the data.

fit <-ses(sales_ts, h=5)fit$model # model parameters

The smoothing algorithm chose \(\alpha\) = 0.5334.

View the forecasted values and corresponding prediction intervals, and plot.

fit # numeric forecast

Point Forecast Lo 80 Hi 80 Lo 95 Hi 95

2019 Q1 1.877535 1.338198 2.416871 1.0526910 2.702378

2019 Q2 1.877535 1.266279 2.488790 0.9426994 2.812370

2019 Q3 1.877535 1.201973 2.553096 0.8443518 2.910717

2019 Q4 1.877535 1.143277 2.611792 0.7545846 3.000484

2020 Q1 1.877535 1.088938 2.666131 0.6714805 3.083589

autoplot(fit) # visual forecast

Best fit of \(\alpha\) or not, clearly simple exponential smoothing does not properly apply to this time series with trend and seasonality. There is no trend or seasonality in the forecast for next year’s values.

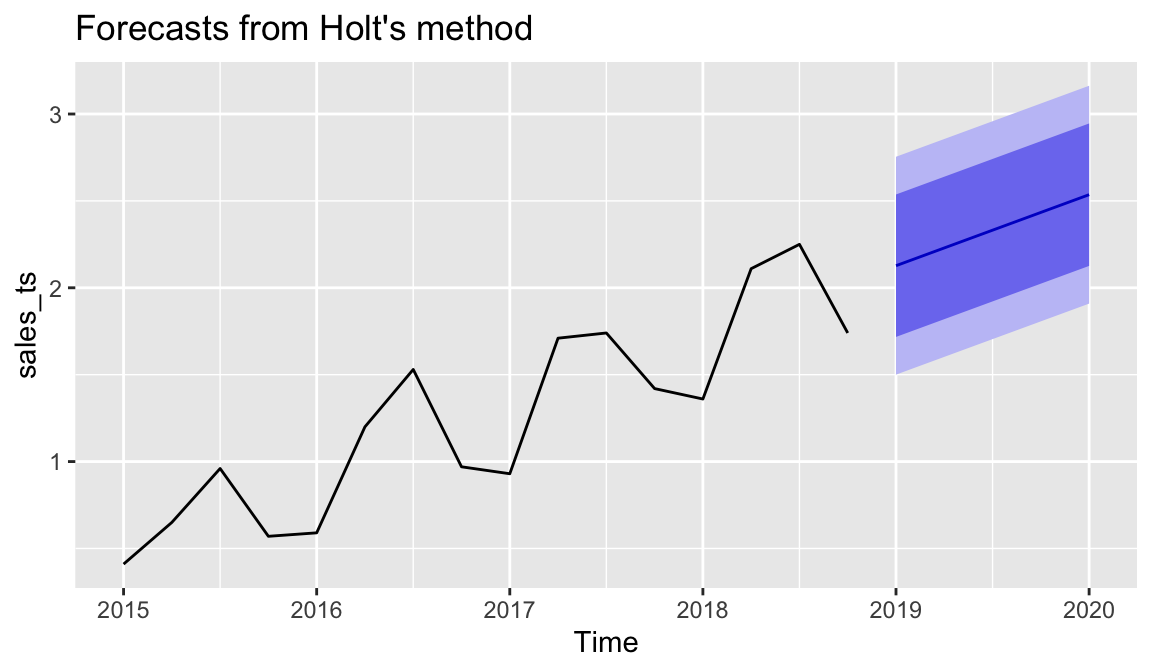

4.4 Exponential Smoothing of Trend

The Holt adaptation of exponential smoothing adds a second parameter, \(\beta\), to account for underlying trend, but not seasonality. Illustrate with the holt() function from the forecast package. View the chosen model parameters.

The value of sigma, the standard deviation of the residuals, decreased from \(s_e=0.450\) for the SES analysis to \(s_e=0.320\) when accounting for linear trend.

fit # numeric forecast

Point Forecast Lo 80 Hi 80 Lo 95 Hi 95

2019 Q1 2.127147 1.717305 2.536989 1.500347 2.753947

2019 Q2 2.229319 1.819476 2.639161 1.602519 2.856119

2019 Q3 2.331490 1.921648 2.741333 1.704691 2.958290

2019 Q4 2.433662 2.023820 2.843504 1.806862 3.060462

2020 Q1 2.535834 2.125991 2.945676 1.909034 3.162634

autoplot(fit) # visual forecast

The Holt method forecast does account for the trend. However, the forecasts still are not optimal because the method does not account for underlying seasonality.

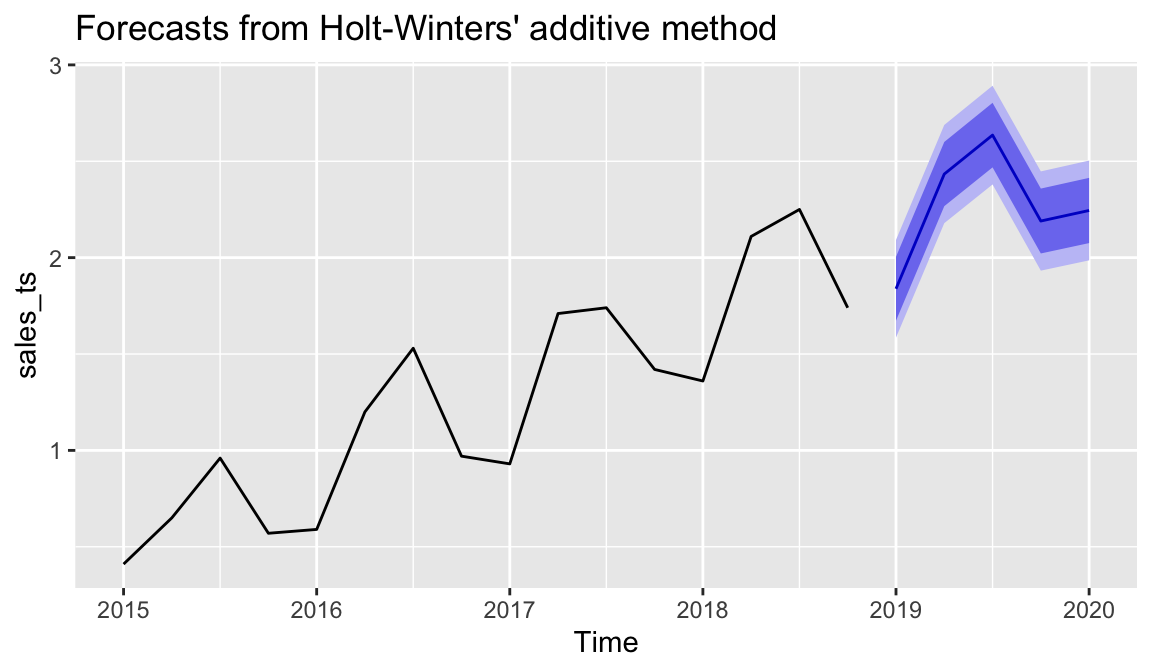

4.5 Exponential Smoothing Trend and Seasonality

Holt-Winters, or triple exponential smoothing, is the preferred smoothing method for data characterized by both trend and seasonality. Use the hw() function from the forecast package.

The value of sigma, the standard deviation of the residuals, decreased from \(s_e=0.450\) for the SES analysis to \(s_e=0.320\) when accounting for linear trend. Accounting for trend and seasonality lowered the standard deviation to \(s_e=0.129\), a substantial and meaningful reduction.

Get the numeric forecasts, prediction intervals, and the visualization.

fit

Point Forecast Lo 80 Hi 80 Lo 95 Hi 95

2019 Q1 1.838427 1.672779 2.004074 1.585091 2.091762

2019 Q2 2.433648 2.267112 2.600184 2.178954 2.688342

2019 Q3 2.635763 2.468341 2.803185 2.379714 2.891813

2019 Q4 2.189985 2.021680 2.358291 1.932584 2.447387

2020 Q1 2.244745 2.075555 2.413935 1.985991 2.503498

autoplot(fit)

The hw function provides two seasonal methods, "additive" and "multiplicative". The default is "additive". To estimate a multiplicative model, set the parameter seasonal to "multiplicative".